What is the Automated Waste Collection System Market Overview – definition, scope, and significance?

The Automated Waste Collection System (AWCS) market comprises technologies that use pneumatic or robotic solutions to transport waste from collection points to a central processing facility without manual handling. The scope includes stationary pipe‑based networks and mobile collection units deployed across various end‑users such as airports, schools, hospitals, corporate offices, and hotels/restaurants. Its significance lies in enhancing hygiene, reducing labor costs, and supporting smart‑city initiatives by optimizing waste logistics and lowering carbon footprints.

What are the main drivers, restraints, challenges, and opportunities in the Automated Waste Collection System Market?

Key drivers include rising urbanization, stricter environmental regulations, and the need for efficient waste management in high‑traffic facilities. Restraints stem from high upfront capital investment and legacy infrastructure compatibility issues. Challenges involve complex retrofitting in dense built‑up areas and limited awareness among smaller operators. Opportunities arise from government incentives for smart‑city projects, advancements in sensor‑based monitoring, and the expansion of AWCS into emerging markets seeking sustainable solutions.

What growth trends are shaping the Automated Waste Collection System Market?

Current trends feature the integration of IoT sensors for real‑time fill‑level monitoring, enabling predictive maintenance and route optimization. There is a shift toward modular, scalable designs that accommodate both stationary pipe networks and mobile units. Additionally, sustainability mandates are prompting companies to pair AWCS with recycling and waste‑to‑energy initiatives, reinforcing the market’s eco‑friendly narrative.

How has COVID‑19 impacted the Automated Waste Collection System Market and what is the recovery trajectory?

The pandemic temporarily slowed new installations due to construction delays and constrained capital spending. However, heightened hygiene awareness accelerated demand for contact‑less waste handling in hospitals and public venues. As economies rebound, the market is experiencing a strong recovery, supported by renewed public‑sector budgets for infrastructure upgrades and a surge in smart‑city funding.

Who are the major competitors and what is the consolidation landscape in the Automated Waste Collection System Market?

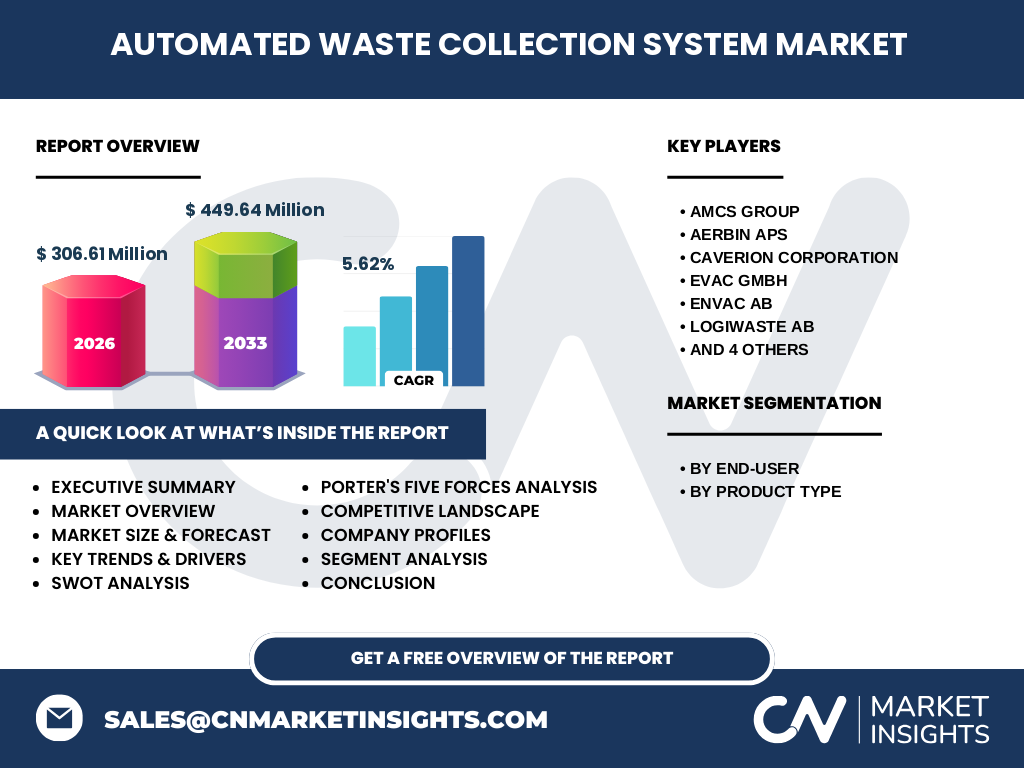

Leading players include AMCS Group, Aerbin APS, Caverion Corporation, EVAC GmbH, Envac AB, Logiwaste AB, MBAT, MEIKO, Marimatic OY, and Stream Environment. The market shows moderate consolidation, with larger firms acquiring niche technology providers to broaden product portfolios and geographic reach. Strategic alliances focus on integrating digital platforms and expanding service networks across key regions.

What are the high‑level findings in the Executive Summary of the Automated Waste Collection System Market?

The market is valued at USD 306.61 million in 2026 and is projected to reach USD 449.64 million by 2033, reflecting a CAGR of 5.62 %. Growth is propelled by sustainability regulations, smart‑city investments, and demand from high‑traffic end‑users. While capital intensity remains a barrier, emerging IoT capabilities and government incentives present strong upside potential for stakeholders.

What are the forecast expectations for the Automated Waste Collection System Market from 2025 to 2032?

Based on the provided CAGR of 5.62 %, the market is expected to continue expanding steadily. Forecasts indicate a progression from the 2026 baseline of USD 306.61 million to approximately USD 449.64 million by 2033. This trajectory underscores persistent demand across both stationary and mobile product segments and suggests accelerating adoption in regions prioritizing smart waste infrastructure.

How is the Automated Waste Collection System Market sized and shared by segmentation?

Segmenting by end‑user, the market serves airports, educational institutions, hospitals, corporate offices, and hotels/restaurants, each benefiting from reduced labor and enhanced hygiene. By product type, the market splits into stationary pipe‑based systems and mobile collection units, with stationary solutions typically dominating large‑scale campuses, while mobile units cater to flexible or retrofitted environments. Detailed numeric shares are not disclosed, but both segments contribute materially to overall growth.

What is the global Automated Waste Collection System market size and share by region?

The worldwide market reached USD 306.61 million in 2026 and is projected to expand to USD 449.64 million by 2033. While specific regional dollar values are not provided, the market’s growth is driven by adoption in North America, Europe, and Asia‑Pacific, where smart‑city initiatives and regulatory pressures are most pronounced. These regions collectively account for the majority of market activity.

What does the regional analysis reveal about Automated Waste Collection System market performance?

North America leads in early adoption due to mature infrastructure and strong environmental policies. Europe follows, propelled by stringent waste‑handling directives and extensive airport and hospital networks. Asia‑Pacific shows rapid uptake, driven by urbanization and government programs supporting smart‑city technologies. Emerging economies in Latin America and the Middle East present nascent opportunities as they modernize waste management.

Which companies are leading in the Automated Waste Collection System market and what are their strategies?

AMCS Group focuses on digital platform integration, offering end‑to‑end waste management solutions. Envac AB leverages its extensive pipe‑network expertise to expand globally. EVAC GmbH emphasizes modular mobile units for flexible deployment. Companies such as Caverion and Aerbin APS pursue strategic partnerships with municipalities to secure long‑term contracts. Innovation, service diversification, and geographic expansion are common strategic themes.

How does Porter’s Five Forces analysis apply to the Automated Waste Collection System market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is low, as components are sourced from multiple manufacturers. Bargaining power of buyers is moderate; large institutions negotiate contracts but value long‑term reliability. Threat of substitutes is limited, given the unique benefits of automated collection over manual methods. Industry rivalry is moderate, with several specialized firms competing on technology and service quality.

What are the SWOT insights for the Automated Waste Collection System market?

Strengths: Enhanced hygiene, labor savings, and alignment with sustainability goals. Weaknesses: High initial cost and integration complexity. Opportunities: IoT integration, government incentives, and expansion into emerging smart‑city projects. Threats: Economic downturns affecting capital expenditure and potential regulatory changes affecting waste‑handling standards.

How is the value chain structured in the Automated Waste Collection System market?

The value chain starts with R&D and component manufacturing (pumps, sensors, control software), followed by system integration and engineering design. Next, project implementation includes site assessment, installation of stationary pipelines or mobile units, and commissioning. Post‑installation services encompass maintenance, data analytics, and upgrade pathways, creating recurring revenue streams for manufacturers and service providers.

What key investment insights can be drawn from the Automated Waste Collection System market?

Investors should prioritize companies with strong IoT capabilities and proven deployment in high‑traffic end‑users, as these segments drive recurring revenue. Funding projects aligned with government smart‑city programs can mitigate risk. Valuation focus on firms that offer integrated service models—hardware, software, and maintenance—as they capture higher lifetime value from clients.

What are the main conclusions and takeaways from the Automated Waste Collection System market analysis?

The market is on a robust growth path, supported by sustainability mandates and technological advances. While capital intensity poses a barrier, the combination of regulatory pressure, smart‑city funding, and IoT‑enabled efficiencies creates a compelling case for adoption. Stakeholders that can deliver turnkey, data‑rich solutions are positioned to capture the expanding opportunity.

How was the research methodology designed for this Automated Waste Collection System market report?

Primary data were gathered through interviews with industry executives, technology providers, and municipal officials. Secondary sources included company filings, trade publications, and government databases. Market sizing employed a top‑down approach anchored to the 2026 base figure, while forecasting applied the disclosed CAGR of 5.62 % to project forward values through 2033.

What is the scope of the research and its limitations?

The study covers global market dynamics, segmentation by end‑user and product type, and regional performance across major geographies. It focuses on publicly available financial data and disclosed market estimates. Limitations arise from the absence of granular regional revenue figures and the reliance on industry‑provided growth rates, which may evolve with macroeconomic shifts.

Which key companies have recent developments in the Automated Waste Collection System market?

AMCS Group announced a partnership with a major European airport to deploy a new pneumatic network. Envac AB launched an upgraded sensor suite for real‑time waste monitoring. EVAC GmbH introduced a compact mobile unit targeting the hospitality sector. Aerbin APS secured a multi‑year contract with a leading university consortium, while Caverion Corporation expanded its service portfolio to include predictive maintenance analytics.